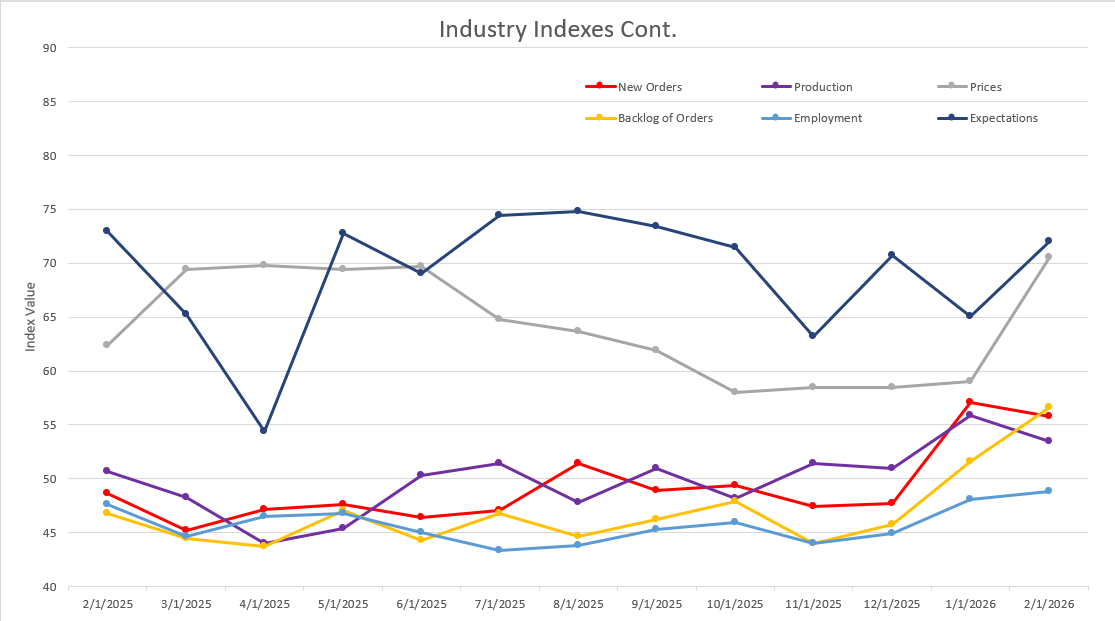

Economic activity in the manufacturing sector expanded in February for the second straight month but only the third time in 40 months, say the nation’s supply executives in the latest ISM® Manufacturing PMI® Report.

The Manufacturing PMI® registered 52.4 percent in February, a 0.2-percentage point decrease compared to the reading of 52.6 in January. The overall economy continued in expansion for the 16th month. (Important data point reference: A Manufacturing PMI reading above 50 percent indicates that the manufacturing economy is generally expanding; below 50 percent indicates that it is generally declining. A Manufacturing PMI above 42.5 percent, over a period of time, indicates that the overall economy, or gross domestic product (GDP), is generally expanding; below 42.5 percent, it is generally declining. The distance from 50 percent or 42.5 percent is indicative of the extent of the expansion or decline.)

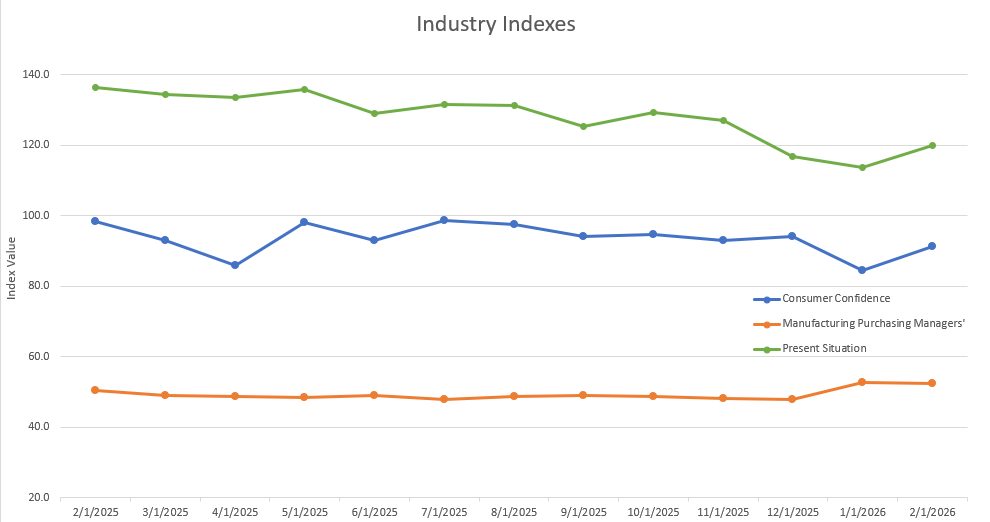

The Conference Board Consumer Confidence Index® increased by 2.2 points in February to 91.2 (1985=100), from an upwardly revised 89.0 in January.

Please see the graphs for other notable indexes related to our industry.

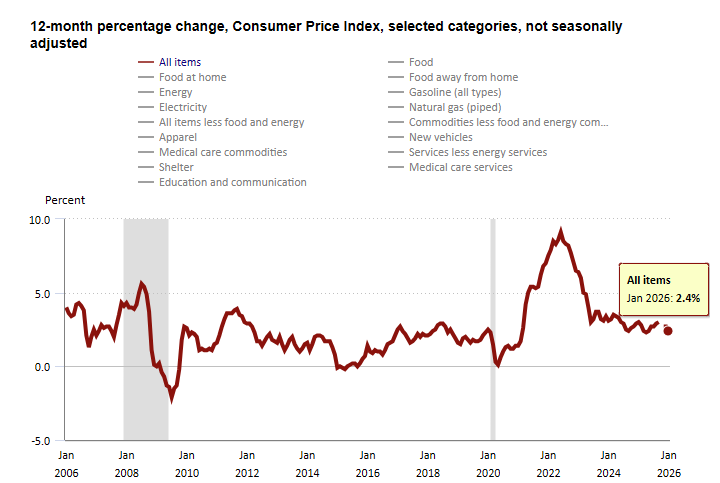

The Consumer Price Index (CPI, otherwise known as our “inflation” friend) is currently at 2.4% in January 2026, down from 2.7% in December 2025. CPI tracks the rate of change in US inflation over time, and the following shows the trends over the past 20 years.

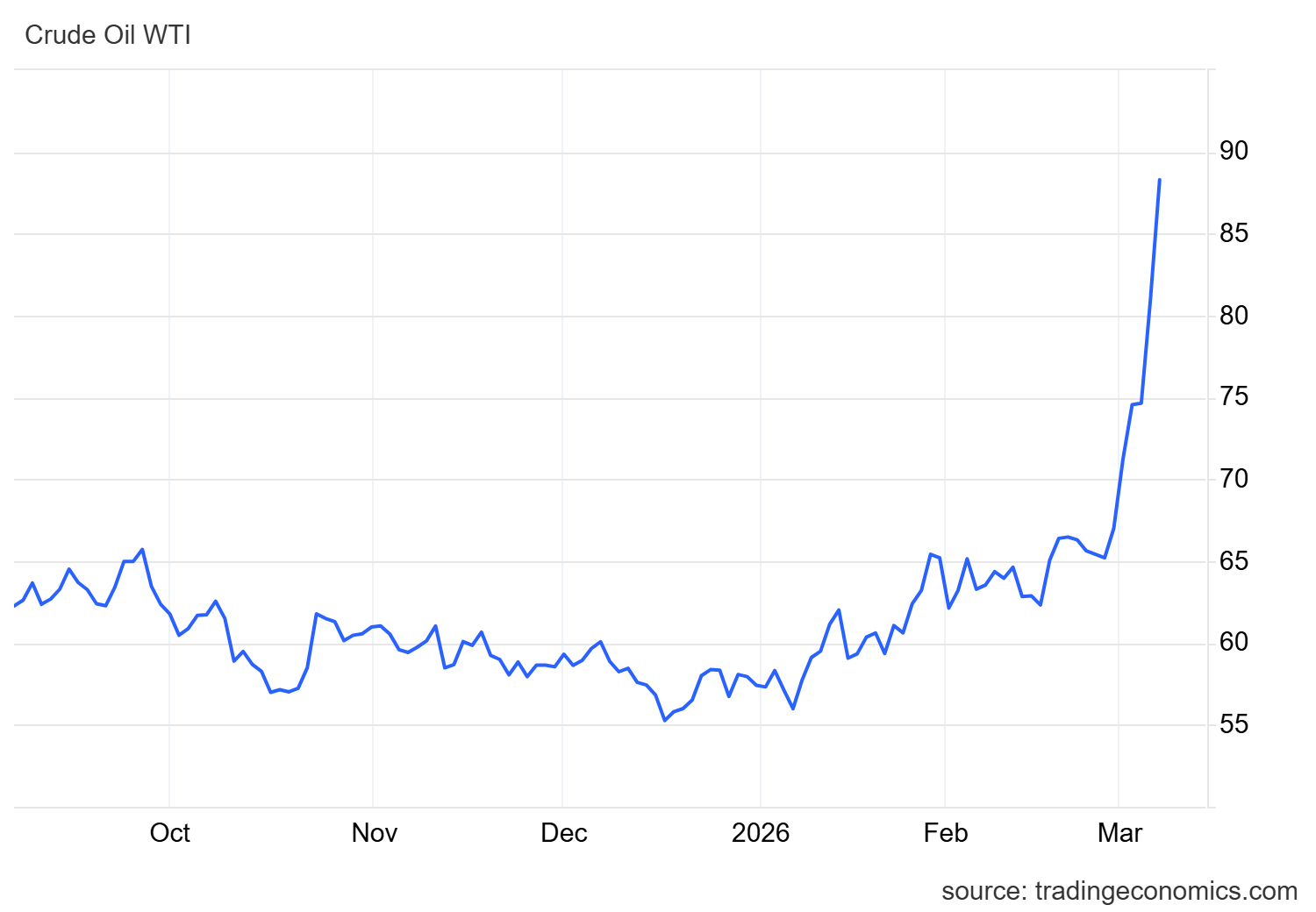

WTI crude oil futures climbed more than 6% to $88 per barrel as of today, after a wild ride yesterday with prices climbing close to $120 per barrel. This week’s biggest jump was on par with the 2022 Russian invasion of Ukraine, as the escalating Middle East conflict continues to severely disrupt global energy flows. Qatar’s Energy Minister Saad al-Kaabi told the Financial Times that Gulf exporters would halt production within days if tankers are unable to pass through the Strait of Hormuz. The strait is a crucial route that normally handles about 20 million barrels of oil and petroleum products per day. Meanwhile, tensions remain high after Abbas Araghchi said Iran was not seeking negotiations. The US signaled possible actions to ease pressure, including the potential release of oil from strategic reserves, while also temporarily allowing India to purchase some Russian crude already at sea. Saudi Arabia raised oil prices for Asian buyers and redirected shipments through Red Sea ports to bypass Hormuz.

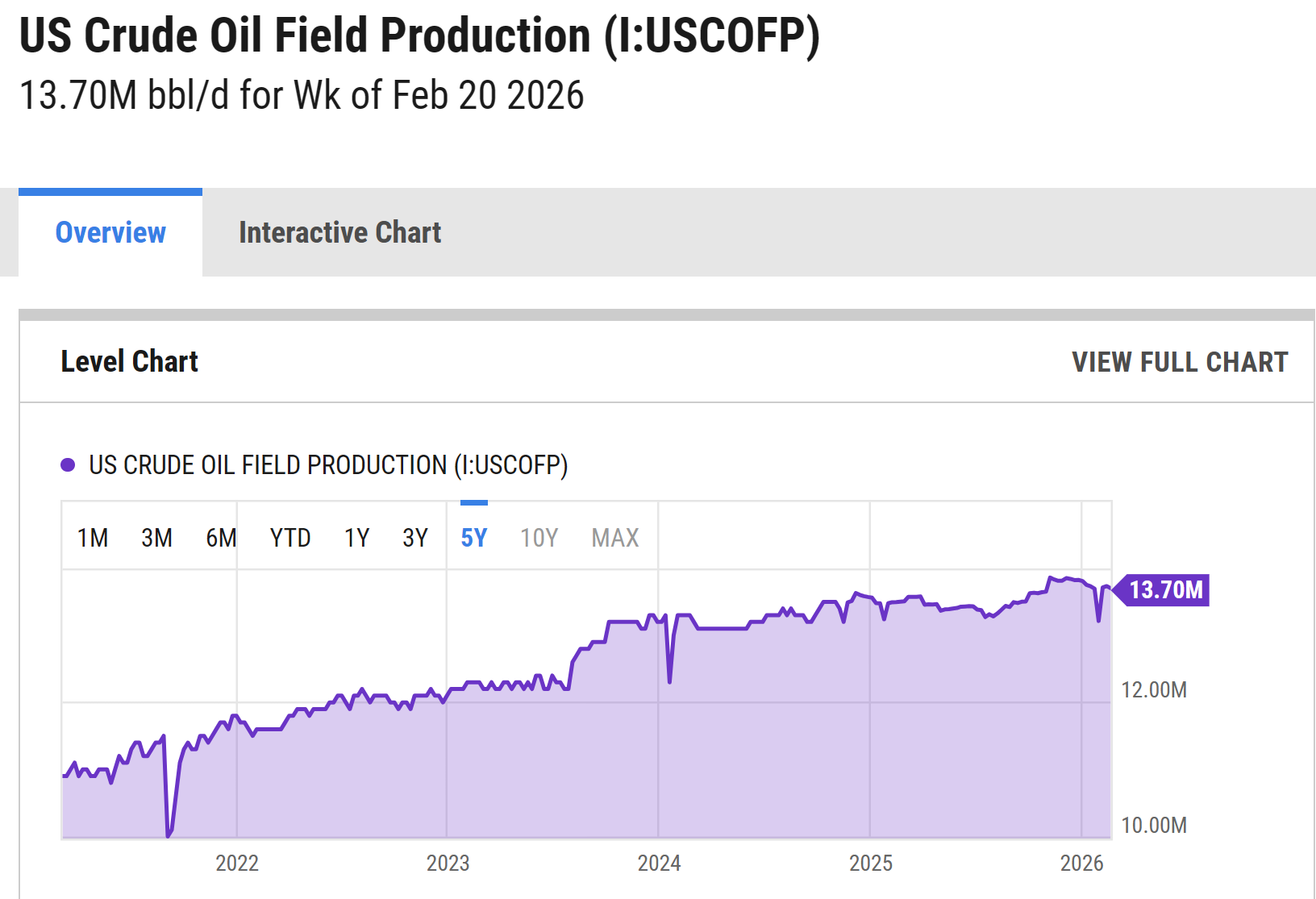

The online US Oil Rig Count is currently reported as 550, which is down 1 compared to last month’s report and down 43 from February 28, 2025. This key and leading indicator shows the current demand for products used in drilling, completing, producing, and processing hydrocarbons, which we all use every day as fuel sources and finished products.

The number of rigs conducting oil and gas drilling in the United States remains stagnant, but efficiency has increased significantly over the years, as shown in the chart below. We are drilling at or near record production levels. However, this trend of fewer rigs still reflects the priority of drillers to focus on efficiency and enhancing shareholder returns rather than expanding production through capital investments due to the previous administration’s desire to move away from fossil fuels. This philosophy might change now that the Trump administration is entirely behind fossil fuels. To provide context, in 2019, 954 rigs were drilling for oil and gas in the US, and, in 2014, there were 1609 rigs before oil prices dropped below $20 per barrel at the end of that year.

Tariffs have tightened, untightened, and will continue to evolve as the Trump administration navigates global negotiations.

Whew… There’s A LOT to unpack here, so hold on for the roller coaster ride.

A little background on where all of this started and what it means. Tariffs are duties placed on foreign goods, paid by domestic importers to Customs and Border Patrol at ports of entry. President Trump introduced tariffs on select Chinese goods in his first term back in 2018, which President Joe Biden later maintained, along with duties on steel and aluminum from most countries. In February of 2025, Trump reinstated tariffs—10% more on Chinese imports, bringing them to 35%, and 25% on Mexican and Canadian goods (except for oil, taxed at 10%).

As of March 10, 2026, at 11 am EST, U.S. tariff policy still remains in flux but is trending tighter across broad categories, with several fast-moving legal and policy developments.

The U.S. tariff landscape shifted rapidly following last Friday’s Supreme Court ruling, creating immediate uncertainty across global metals markets and supply chains. While headlines suggested tariffs were struck down, the practical reality is more nuanced. Tariffs remain in place, but under a new legal authority.

On February 20, 2026, the Supreme Court ruled that tariffs imposed under the International Emergency Economic Powers Act (IEEPA) exceeded presidential authority. The Court determined that IEEPA does not grant the executive branch the power to impose broad tariffs, reaffirming that tariff authority primarily resides with Congress.

The decision invalidated the legal basis for several global tariffs and temporarily raised expectations that import duties could be reduced or removed. That expectation proved to be short-lived. Within hours of the ruling, the administration enacted tariffs under Section 122 of the Trade Act of 1974.

This provision allows the president to impose temporary import surcharges of up to 15 percent for 150 days without congressional approval to address balance of payments or trade concerns.

The new policy now establishes a 10 percent global tariff surcharge on most imported goods. While structured differently from the previous tariffs, the economic impact for industrial buyers is largely similar.

For the metals and heavy manufacturing sectors, the tariff framework now includes multiple overlapping mechanisms:

- First off, a 10 percent global tariff under Section 122 (under temporary authority as mentioned earlier)

- The Section 232 steel and aluminum tariffs remain fully in force at 50%

- Section 301 China tariffs will continue unchanged

- USMCA-compliant goods from Canada and Mexico remain mostly exempt

- And, select energy and critical mineral exemptions continue

In practical terms, the Supreme Court ruling changed the legal pathway, not the protectionist posture of U.S. trade policy. Because Section 122 authority expires after 150 days, markets now face a defined policy clock. The administration is widely expected to use this window to transition tariffs into longer-term trade actions under Sections 301 or 232 that are more legally durable.

What Comes Next. Over the next several months, industry participants should watch for:

- New country-specific trade investigations

- The Expansion of national security-based tariffs

- And, Congressional involvement in extending tariff authority

As we’ve already seen, litigation over tariff refunds tied to the invalidated measures are now underway. This will get a little sticky as seen in Justice Brett Kavanaugh’s dissenting opinion. He warned that issuing refunds would be complex, particularly because many importers have already passed those costs on to consumers.

Here’s the Bottom Line – Despite a major Supreme Court decision, tariffs impacting the metals sector remain firmly in place. The legal foundation has changed, but the operating environment for manufacturers, fabricators, and equipment producers has not materially eased.

For now, the metals market remains in a tariff-driven pricing environment with elevated uncertainty and a likely continuation of trade protection measures through at least mid-2026.

How does this affect your pricing for pressure vessels and heat exchangers?

At Ward, we purchase 80-90% domestically, depending upon the project. This means our total material spend has increased by approximately 5-15% since the tariffs were enacted, resulting in a 3-10% overall unit price increase after labor is factored in. We are doing our part to support American manufacturing while keeping our pricing as competitive as possible.

The administration has published several tariff fact sheets on the White House website (click here) as the tariff topic has evolved.

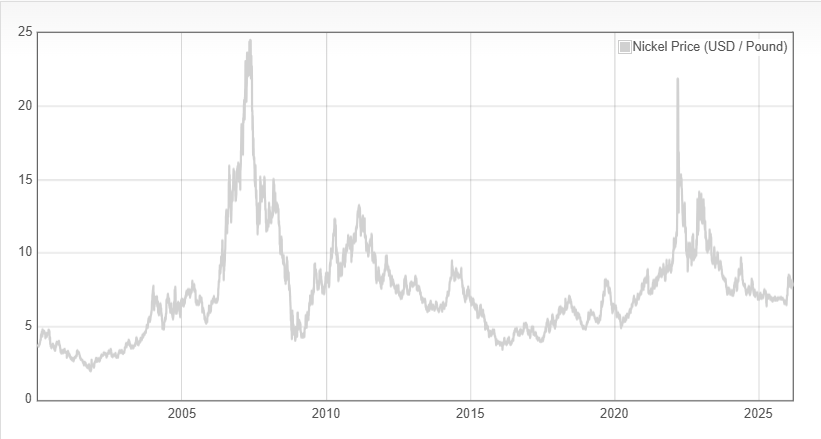

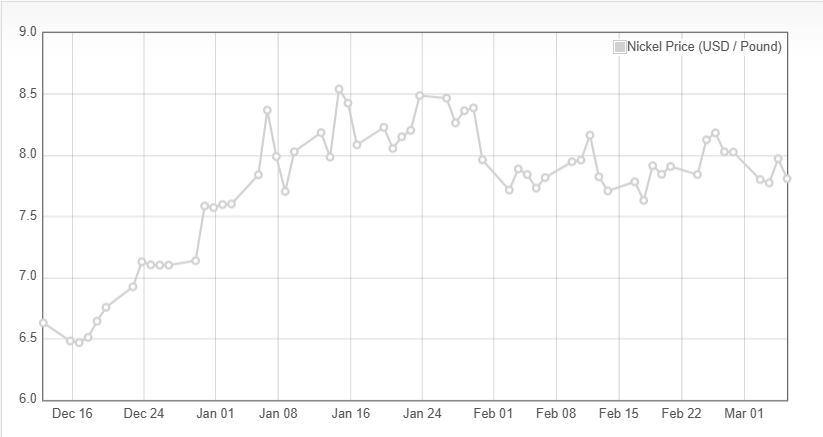

Nickel futures fell to around $7.801 per pound in early March, tracking the pullback for other industrial metals as heightened geopolitical tensions in the Middle East triggered risk-off flows across the manufacturing sector. Iran’s threat to close the Strait of Hormuz drove oil prices sharply higher, strengthening the dollar and prompting investors to trim exposure to cyclical commodities. Market participants remain cautious, reacting to heightened risk sentiment. Meanwhile, on the supply side, Indonesia’s 2026 ore quota cap at 270 million wet metric tons and enforcement against illegal mining continue to limit tightness. New project ramp-ups, including PT Vale’s Pomalaa initial ore sales, signal steady feedstock availability. Firm Philippine ore offers support to upstream costs, but broader expansion in refined nickel output has restrained upside.

Plate mill plate lead times (weeks):

Domestic:

Stainless & Duplex: 9 to 10 (previously 6 to 8)

Nickel Alloys: 8 to 13 (previously 6 to 13)

Carbon steel: 6 to 8 (no change)

*Keep in mind, some plates will exceed the estimated ranges depending on the mill’s production schedule and slab availability. *

Welded tubing lead times (weeks):

Domestic:

Carbon: 6 to 16 (no change)

Stainless: 8 to 15 (no change)

Nickel Alloy: 8 to 18 (no change)

Import:

Carbon: 14 to 25 (no change)

Stainless: 16 to 30 (no change)

Nickel Alloy: 16 to 42 (no change)

Seamless tubing lead times (weeks):

Domestic:

Carbon: 6 to 26 (no change)

Stainless: 8 to 26 (no change)

Nickel Alloy: 8 to 18 (no change)

*Lead times are accurate if bar is in stock. If not, lead times can increase to 44 weeks as most bars are of foreign melt. *

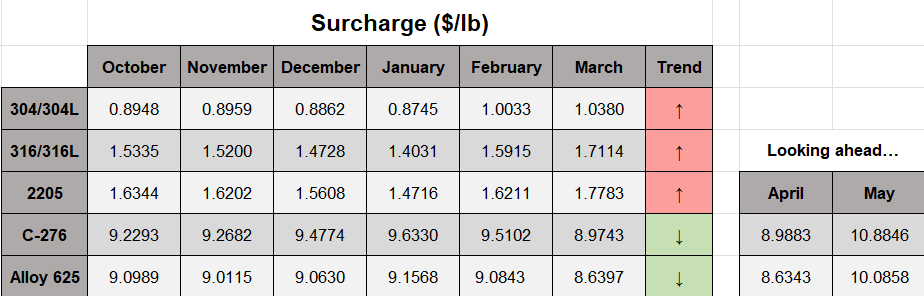

Nickel Prices have had an interesting ride over the past three decades, with a low of $2.20/lb. in October 2001 (following the September 11 events) and a high of $23.72/lb. in May 2007. Surcharges trail Nickel prices by approximately two months, so they would have been at their lowest in December 2001 (304 was $0.0182/lb.) and peak in July 2007 (304 was $2.2839/lb.).