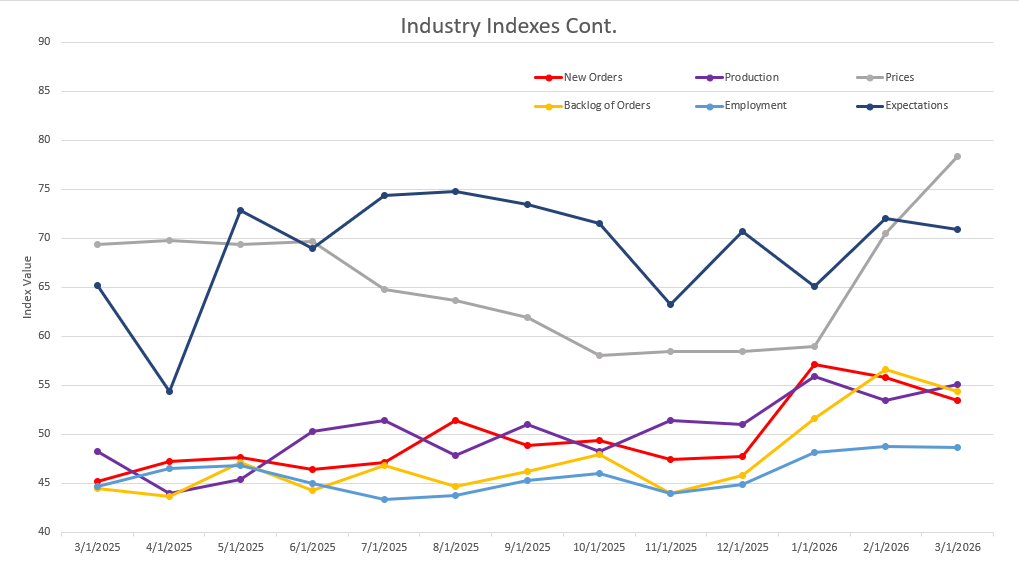

Economic activity in the manufacturing sector expanded in March for the third consecutive month, say the nation’s supply executives in the latest ISM® Manufacturing PMI® Report.

The Manufacturing PMI® registered 52.7 percent in March, a 0.3-percentage point increase compared to the reading of 52.4 percent in February. The overall economy continued in expansion for the 17th month in a row. (Important data point reference: A Manufacturing PMI reading above 50 percent indicates that the manufacturing economy is generally expanding; below 50 percent indicates that it is generally declining. A Manufacturing PMI above 42.5 percent, over a period of time, indicates that the overall economy, or gross domestic product (GDP), is generally expanding; below 42.5 percent, it is generally declining. The distance from 50 percent or 42.5 percent is indicative of the extent of the expansion or decline.)

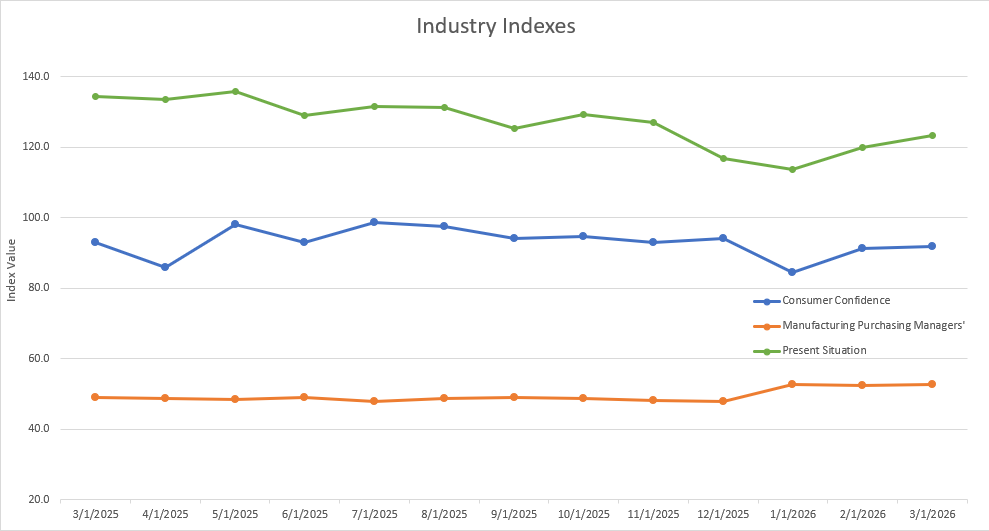

The Conference Board Consumer Confidence Index® edged up by 0.8 points in March to 91.8 (1985=100), from 91.0 in February.

Please see the graphs for other notable indexes related to our industry.

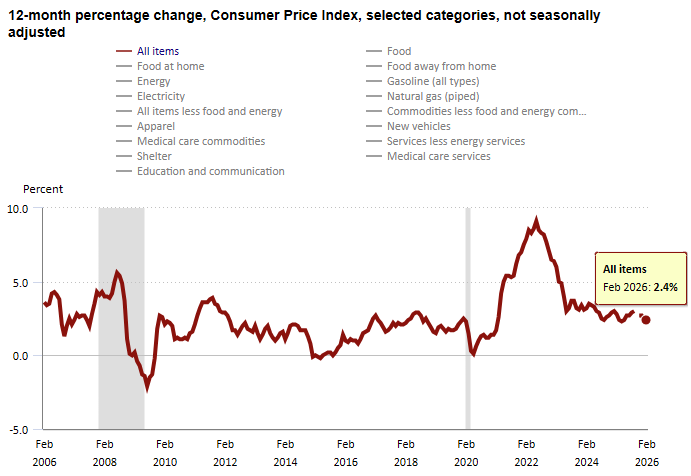

The Consumer Price Index (CPI, otherwise known as our “inflation” friend) is currently at 2.4% in February 2026, the same as in January 2026. CPI tracks the rate of change in US inflation over time, and the following shows the trends over the past 20 years.

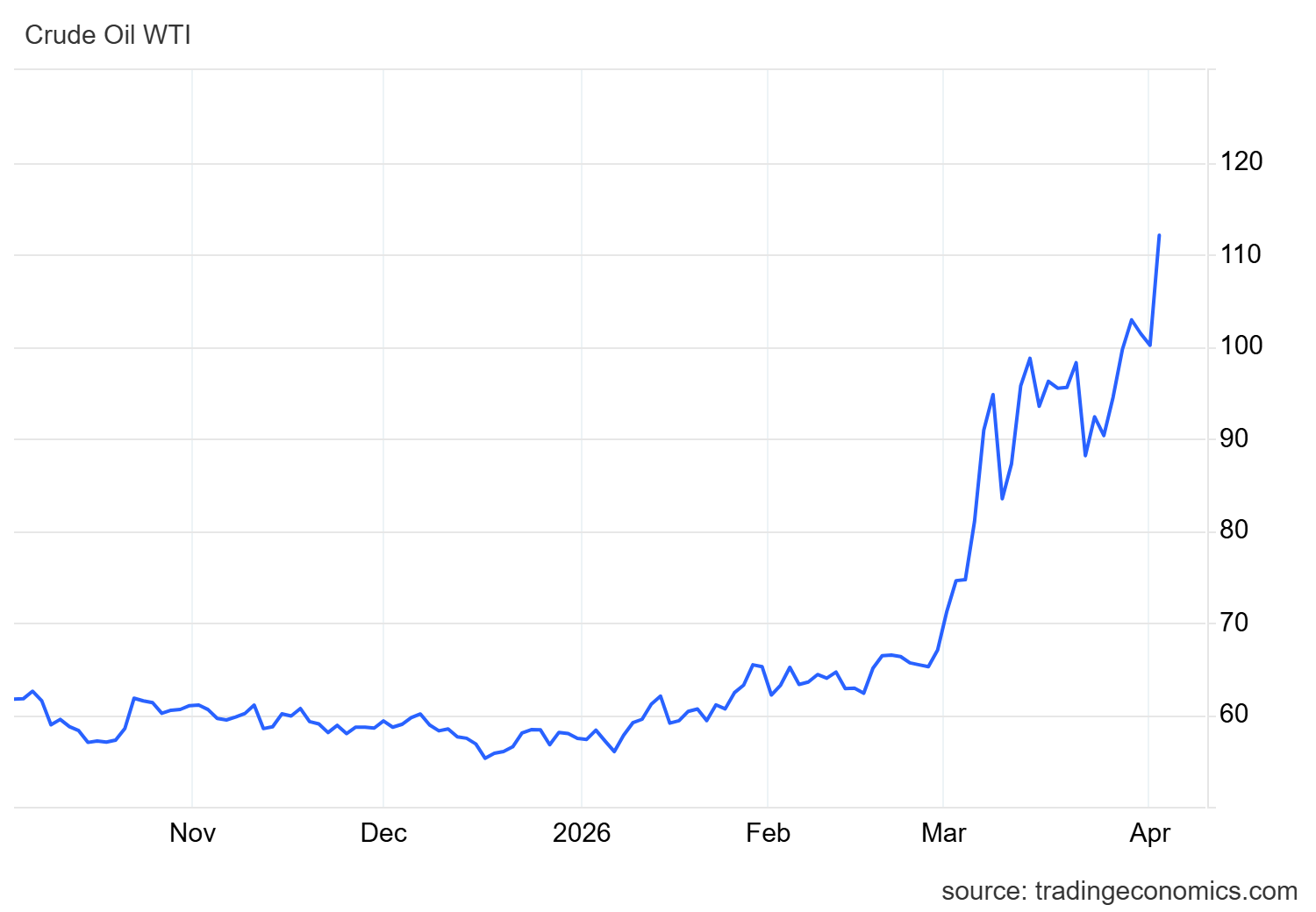

WTI crude oil futures soared 11% to cross $111 per barrel on Thursday, the highest in nearly four years, regaining traction on a volatile session as markets reconsidered the magnitude of supply risks from the ongoing war in the Persian Gulf. US President Trump pledged to escalate attacks on Iran and its infrastructure in the coming weeks if Tehran does not accept American ceasefire conditions, prompting Tehran to retaliate against the aggressive rhetoric. Earlier in the session, oil prices had eased on reports that Oman and Iran were coordinating a toll for tankers crossing the Hormuz chokepoint, but optimism about a normalized supply outlook was short-lived. Consequently, dated Brent benchmarks rose to past $140 per barrel, the highest since 2008. Meanwhile, the UK is hosting talks with dozens of countries to secure the route, while OPEC+ is considering a potential output increase, though any additional supply is unlikely to affect markets in the near term.

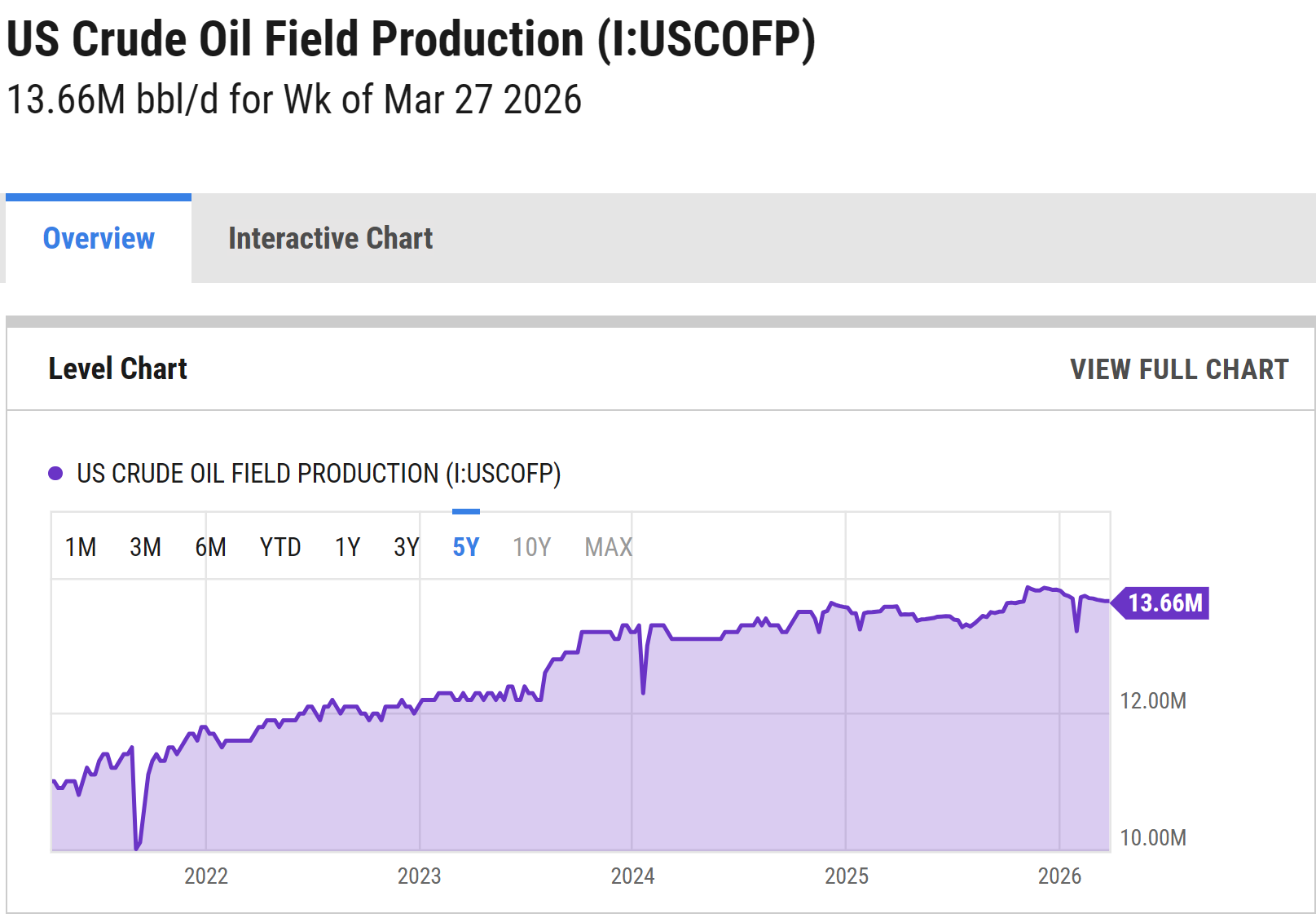

The online US Oil Rig Count is currently reported as 548, which is down 2 compared to last month’s report and down 42 from April 04, 2025. This key and leading indicator shows the current demand for products used in drilling, completing, producing, and processing hydrocarbons, which we all use every day as fuel sources and finished products.

The number of rigs conducting oil and gas drilling in the United States remains stagnant, but efficiency has increased significantly over the years, as shown in the chart below. We are drilling at or near record production levels. However, this trend of fewer rigs still reflects the priority of drillers to focus on efficiency and enhancing shareholder returns rather than expanding production through capital investments due to the previous administration’s desire to move away from fossil fuels. This philosophy might change now that the Trump administration is entirely behind fossil fuels. To provide context, in 2019, 954 rigs were drilling for oil and gas in the US, and, in 2014, there were 1609 rigs before oil prices dropped below $20 per barrel at the end of that year.

Tariffs have tightened, untightened, and will continue to evolve as the Trump administration navigates global negotiations.

Whew… There’s still A LOT to unpack here, so hold on for the roller coaster ride.

A little background on where all of this started and what it means. Tariffs are duties placed on foreign goods, paid by domestic importers to Customs and Border Patrol at ports of entry. President Trump introduced tariffs on select Chinese goods in his first term back in 2018, which President Joe Biden later maintained, along with duties on steel and aluminum from most countries. In February of 2025, Trump reinstated tariffs—10% more on Chinese imports, bringing them to 35%, and 25% on Mexican and Canadian goods (except for oil, taxed at 10%).

As of April 8th, 2026, at 11 am EST, here’s what we’re seeing. On April 2nd, Trump signed a new proclamation that took effect on April 6th to ultimately counter the February 20, 2026, Supreme Court ruling that stated that tariffs imposed under the International Emergency Economic Powers Act (IEEPA) exceeded presidential authority. The Court determined that IEEPA does not grant the executive branch the power to impose broad tariffs, reaffirming that tariff authority primarily resides with Congress. The Trump administration imposed a brief 10% Section 122 tariff after this ruling, which has now been replaced by the following. Please refer to our March Metal Market Update for more information on the Supreme Court ruling and what has transpired since then.

1 – Section 232 tariff calculation methodology has been overhauled. Tariffs now apply to the full customs value of imported steel, aluminum, and copper products, rather than just the metal portion. This is a major shift from prior methodology.

2 – New tiered rate structure:

Articles made entirely or almost entirely of steel, aluminum, or copper pay a flat 50% on their full value (e.g., steel coils, aluminum sheet). Derivative articles substantially made of these metals pay a flat 25% on their full value. Certain metal-intensive industrial equipment and electrical grid equipment pay 15% through 2027. Products manufactured abroad using 100% U.S.-origin metals are subject to a reduced 10%.

Products containing 15% or less of steel, aluminum, or copper by value are no longer subject to Section 232 tariffs at all.

3 – Copper added to Section 232. In July 2025, President Trump issued a proclamation adding copper to the Section 232 tariffs program at the same 50% rate as steel and aluminum. This is now fully baked into the new framework.

4 – The Section 122 “150-day clock” discussed above and from our March newsletter has been effectively bypassed. The administration has now re-anchored these tariffs to Section 232, which is more legally durable in the long term.

How Does This Affect Imported Pressure Vessels and Heat Exchangers?

Per our understanding, pressure vessels and heat exchangers are fabricated equipment classified under HTS Chapter 84 (industrial machinery), not Chapters 72–76 (raw steel mill products). This distinction matters significantly under the April 6th Section 232 overhaul.

For aluminum heat exchangers, the picture is clear. HTS subheadings 8419.50.10 and 8419.50.50 are explicitly listed as aluminum derivative articles in the April 6th proclamation, meaning imported finished aluminum heat exchangers are subject to a 25% tariff on the full customs value of the unit — not just the metal content. On a $500,000 imported aluminum heat exchanger, the tariff base is the full $500,000.

For stainless steel, alloy, and carbon steel heat exchangers, and for pressure vessels of any material, the situation is less settled. These products typically classify under HTS 8419.50.50 and 8419.89, respectively, neither of which appears in the steel derivatives section of the April 6th annexes. This creates a genuine gray area because imported finished steel heat exchangers and pressure vessels may not currently be explicitly covered by the Section 232 derivative tariff on the finished unit.

It is also worth noting what the Annex language does, and does not, say about tanks and vessels under Chapter 73. Two codes are listed under Annex I-A at the 50% rate:

- HTS 7309.00.00 — “Iron or steel, reservoirs, tanks, vats, similar containers for any material (other than compressed or liquefied gas), with a capacity exceeding 300 l, whether or not lined or heat-insulated, but not fitted with mechanical or thermal equipment”.

- HTS 7311.00.00 — “Iron or steel, containers for compressed or liquefied gas”.

While these codes may appear to cover pressure vessels and storage vessels at first glance, the critical limitation in 7309 is the phrase “not fitted with mechanical or thermal equipment.” A fabricated ASME pressure vessel with nozzles, instrumentation, internals, and process connections would almost certainly not qualify under this language. Similarly, neither code uses the word “vessel” at all, and a purpose-engineered ASME Code vessel is fundamentally different from a simple storage tank or container. The customs classification of fabricated pressure equipment under Chapter 73 versus Chapter 84 is a fact-specific determination, and Chapter 84 typically governs process equipment of this nature.

- What is unambiguous for all product types is that the raw material inputs (i.e. stainless plate, carbon steel plate, seamless and welded tubing, and pipe fittings) are covered at the full 50% rate under Annex I-A, regardless of how the finished equipment is ultimately classified.

As manufacturers of pressure vessels and heat exchangers, we need to continue engaging with our elected officials to ensure that protection is in place for us, manufacturers of steel products, not just for our domestic suppliers.

How does this affect your pricing for pressure vessels and heat exchangers?

At Ward, we purchase 80-90% domestically, depending upon the project. This means our total material spend has increased by approximately 5-15% since the tariffs were enacted, resulting in a 3-10% overall unit price increase after labor is factored in. We are doing our part to support American manufacturing while keeping our pricing as competitive as possible.

The administration has published several tariff fact sheets on the White House website (click here) as the tariff topic has evolved.

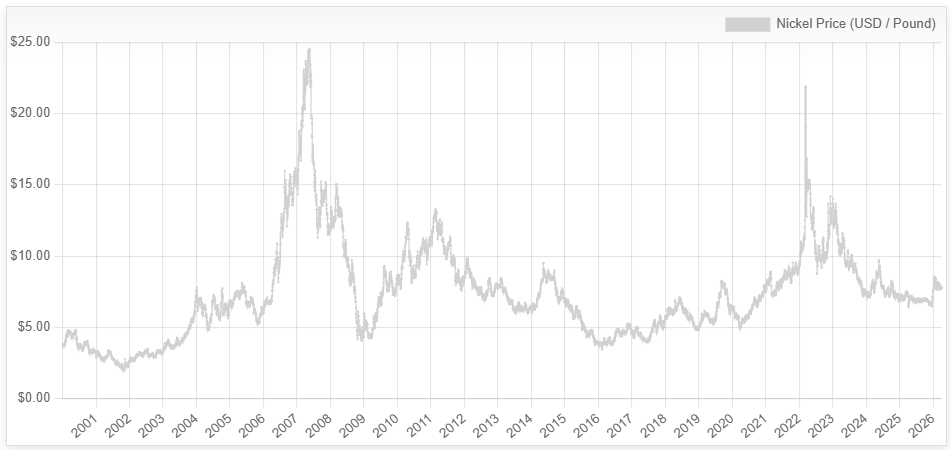

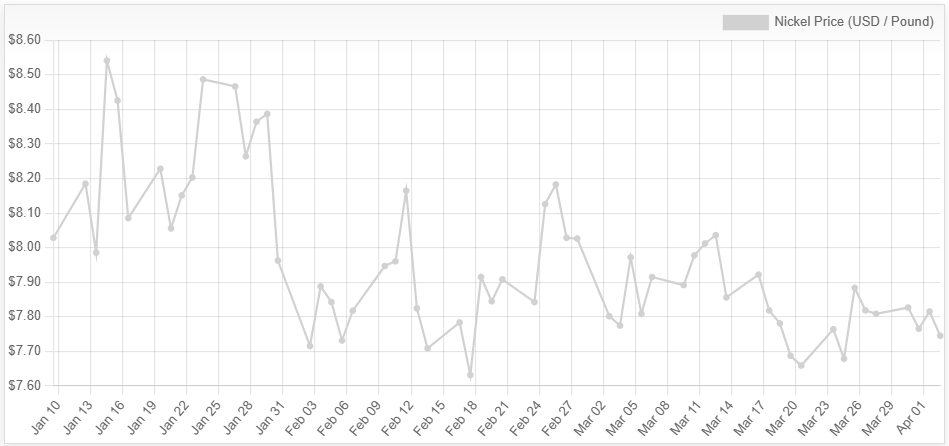

Nickel futures are trading around $7.802 per pound, falling from March highs near $8.060 per pound, reflecting ongoing structural tightness in the market and cautious investor sentiment. Supply remains constrained as Indonesia advances its proposed export tax on nickel, while disruptions to shipping through the Strait of Hormuz add logistical pressure on key raw materials. On the corporate front, Vale Base Metals reported a 13% increase in its nickel reserves and resources in 2025, supporting medium-term supply potential, while regional collaboration through the IndoPhil Nickel Corridor aims to strengthen integrated, resilient supply chains. Demand fundamentals remain robust, driven by growth in electric vehicle batteries, renewable energy storage, and industrial applications. China continues to account for a significant share of exports, while diversification efforts across Asia underscore the strategic importance of nickel in global critical mineral markets.

Plate mill plate lead times (weeks):

Domestic:

Stainless & Duplex: 10 to 11 (previously 9 to 10)

Nickel Alloys: 8 to 15 (previously 8 to 13)

Carbon steel: 6 to 8 (no change)

*Keep in mind, some plates will exceed the estimated ranges depending on the mill’s production schedule and slab availability.*

Welded tubing lead times (weeks):

Domestic:

Carbon: 6 to 16 (no change)

Stainless: 8 to 15 (no change)

Nickel Alloy: 8 to 18 (no change)

Import:

Carbon: 14 to 25 (no change)

Stainless: 16 to 30 (no change)

Nickel Alloy: 16 to 42 (no change)

Seamless tubing lead times (weeks):

Domestic:

Carbon: 6 to 26 (no change)

Stainless: 8 to 26 (no change)

Nickel Alloy: 8 to 18 (no change)

*Lead times are accurate if bar is in stock. If not, lead times can increase to 44 weeks as most bars are of foreign melt. *

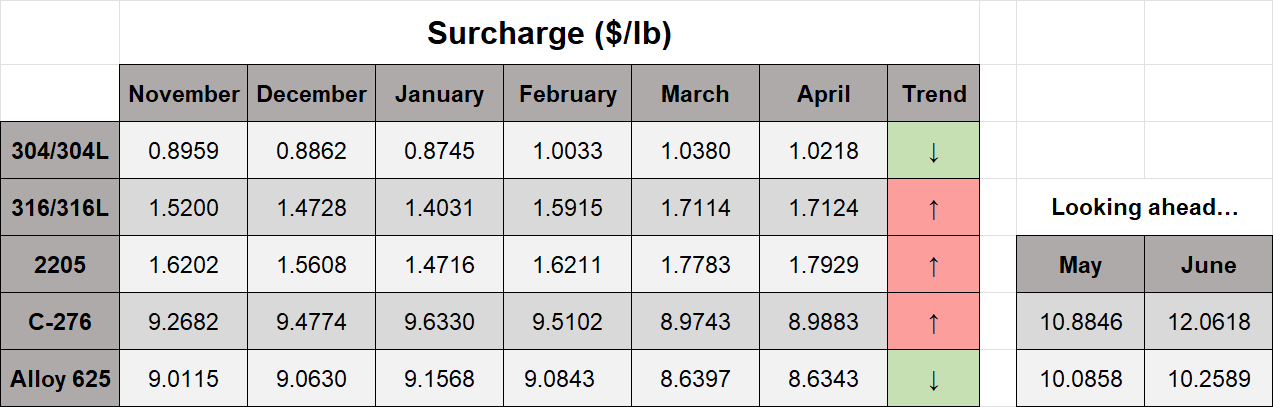

Nickel Prices have had an interesting ride over the past three decades, with a low of $2.20/lb. in October 2001 (following the September 11 events) and a high of $23.72/lb. in May 2007. Surcharges trail Nickel prices by approximately two months, so they would have been at their lowest in December 2001 (304 was $0.0182/lb.) and peak in July 2007 (304 was $2.2839/lb.).