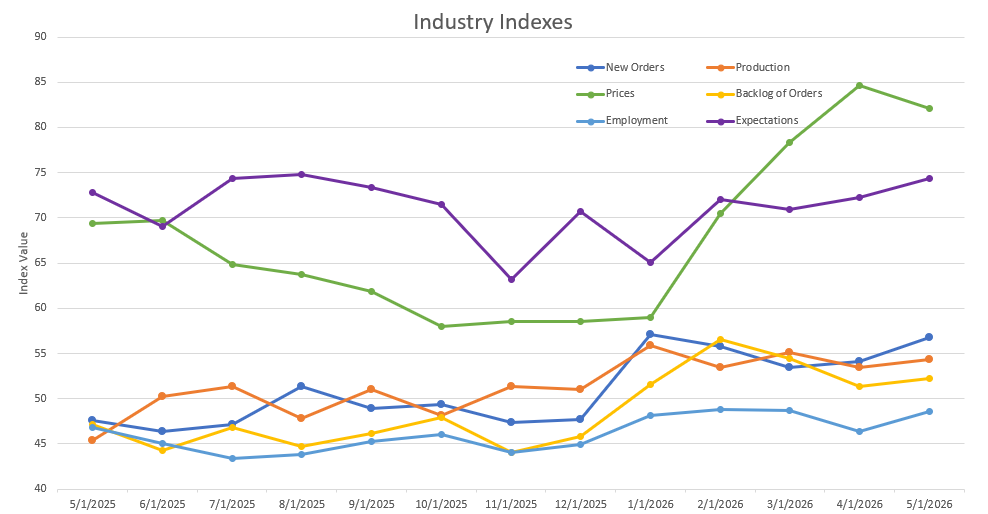

Economic activity in the manufacturing sector expanded in May for the fifth consecutive month, say the nation’s supply executives in the latest ISM® Manufacturing PMI® Report.

The Manufacturing PMI® registered 54 percent in May, 1.3 percentage points higher than in April and its highest reading since May 2022 (55.9 percent). The overall economy continued in expansion for the 19th month in a row. (Important data point reference: A Manufacturing PMI reading above 50 percent indicates that the manufacturing economy is generally expanding; below 50 percent indicates that it is generally declining. A Manufacturing PMI above 42.5 percent, over a period of time, indicates that the overall economy, or gross domestic product (GDP), is generally expanding; below 42.5 percent, it is generally declining. The distance from 50 percent or 42.5 percent is indicative of the extent of the expansion or decline.)

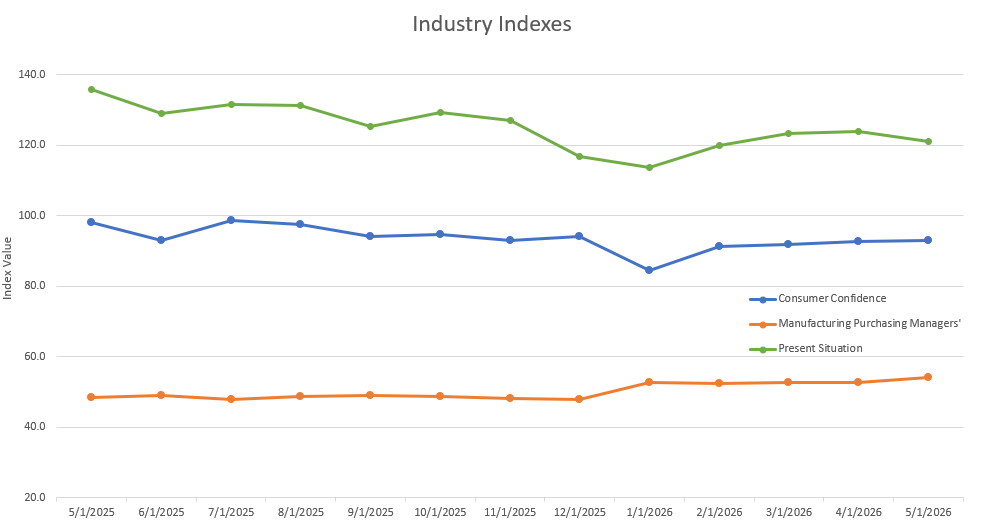

The Conference Board Consumer Confidence Index® dipped 0.7 points to 93.1 (1985=100) in May, down from an upwardly revised 93.8 in April.

Please see the graphs for other notable indexes related to our industry.

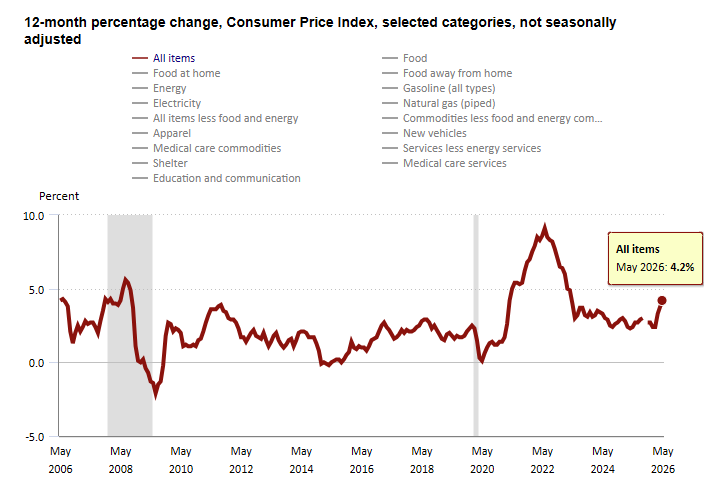

The Consumer Price Index (CPI, otherwise known as our “inflation” friend) is currently at 4.2% in May 2026, up from 3.8% in April 2026 and up from 3.3% in March 2026. CPI tracks the rate of change in US inflation over time, and the following shows the trends over the past 20 years. This is the highest annual increase since May 2023 with energy costs being the big driver of this bump.

WTI crude oil futures eased to $91 per barrel after having crossed $95 earlier on Monday after Iran stated it had ended its military operations against Israel. US President Trump added that both countries were close to a new ceasefire and that there was progress between Washington and Tehran, easing concerns that the escalation would hamper negotiations that gradually restore exports of oil through the Persian Gulf. Still, Israel refrained from signaling their de-escalation, after the first strikes between Iran and Israel since their ceasefire had driven oil futures to surge at the start of the week. Separately, OPEC+ approved another increase in July oil production quotas of 188,000 barrels per day despite persistent supply risks stemming from tensions in the Middle East. Fresh data indicating an aggressive pullback in imports by China also limited supply pressures, as Asia’s top consumer has relied on inventory instead of overseas supply since the start of the conflict.

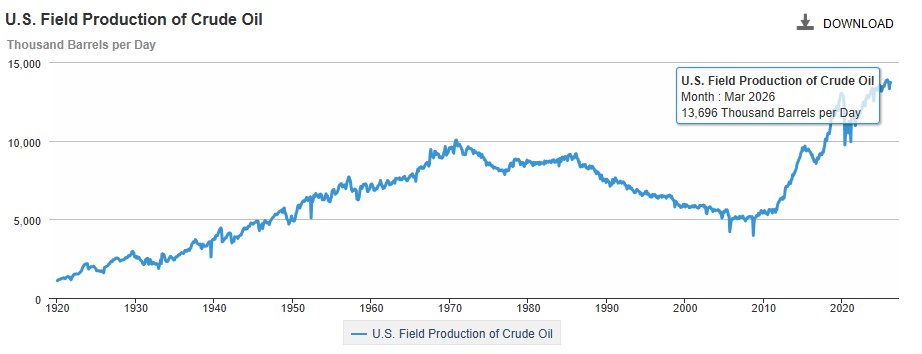

The online US Oil Rig Count is currently reported as 563, which is up 16 compared to last month’s report and up 4 from April 04, 2025. This key and leading indicator shows the current demand for products used in drilling, completing, producing, and processing hydrocarbons, which we all use every day as fuel sources and finished products.

The number of rigs conducting oil and gas drilling in the United States remains stagnant, but efficiency has increased significantly over the years, as shown in the chart below. We are drilling at or near record production levels. However, this trend of fewer rigs still reflects the priority of drillers to focus on efficiency and enhancing shareholder returns rather than expanding production through capital investments due to the previous administration’s desire to move away from fossil fuels. This philosophy might change now that the Trump administration is entirely behind fossil fuels. To provide context, in 2019, 954 rigs were drilling for oil and gas in the US, and, in 2014, there were 1609 rigs before oil prices dropped below $20 per barrel at the end of that year.

Tariffs have tightened, untightened, and will continue to evolve as the Trump administration navigates global negotiations.

Whew… There’s still A LOT to unpack here, so hold on for the roller coaster ride.

A little background on where all of this started and what it means. Tariffs are duties placed on foreign goods, paid by domestic importers to Customs and Border Protection at ports of entry. President Trump introduced tariffs on select Chinese goods in his first term back in 2018, which President Joe Biden later maintained, along with duties on steel and aluminum from most countries. In February of 2025, Trump reinstated tariffs—10% more on Chinese imports, bringing them to 35%, and 25% on Mexican and Canadian goods (except for oil, taxed at 10%). From there, it has been an ever-changing environment with tariffs going up and down from month to month based upon negotiations with other nations.

Tariff Update for June 2026

The tariff landscape continues to move fast. Here is what has changed since last month and what it means for you.

The Section 122 Ruling Stands

As we reported in May, the U.S. Court of International Trade struck down the administration’s 10% global tariff under Section 122 as unlawful. The administration appealed, but the clock is running regardless. Section 122 expires July 24th by statute. It is going away.

What Comes After Section 122… the bridge to Section 301

This is the most important development this month. The administration is not letting reciprocal tariffs die with Section 122. On June 2nd, USTR announced proposed new tariffs under Section 301 covering 60 countries and the European Union, grounded in a forced labor investigation. Proposed rates run from 10% to 12.5% depending on the country. A public hearing is scheduled for July 7th, which is no coincidence. That date tracks directly to the Section 122 expiration. This is the replacement vehicle, and unlike Section 122, Section 301 tariffs can remain in force for four years before mandatory review. The administration found more durable legal ground.

The current proposal includes an exemption for goods already covered under Section 232. That protects our raw material inputs from being double hit. For finished pressure vessels and heat exchangers still sitting in the Chapter 84 classification gray area, the picture is less settled.

The public comment period closes July 6th. That is one day before the hearing. If you believe American pressure vessel and heat exchanger fabricators deserve the same protection afforded to our domestic raw material suppliers, this is a direct and immediate opportunity to put that on the record. We encourage every customer, supplier, and industry partner to file a comment or contact their elected representatives before that deadline.

Section 232 Stands

None of the above pertains to Section 232, which governs tariffs on steel, aluminum, and copper. It was written specifically to authorize tariff action on national security grounds. It has survived every legal challenge to date and remains fully in effect.

The April 6th framework remains the operative structure:

- Raw mill products, plate, sheet, tube, pipe, and fittings at 50% on the full customs value.

- Derivative articles substantially made of steel, aluminum, or copper at 25% on full customs value.

- Certain metal-intensive industrial equipment at a temporary 15% through December 31, 2027.

- Products made with 100% U.S.-origin metal at 10%.

- Products with 15% or less metal content by weight are not subject to Section 232 tariffs.

A new proclamation that took effect June 8th provides targeted relief for select downstream industries. Agricultural equipment, certain residential HVAC systems, and mobile industrial equipment from qualifying trade agreement countries now receive a temporary reduced rate of 15% through December 31, 2027. That does not directly affect pressure vessels or heat exchangers.

How Does This Affect Imported Pressure Vessels and Heat Exchangers?

Per our understanding, pressure vessels and heat exchangers are fabricated equipment classified under HTS Chapter 84 (industrial machinery), not Chapters 72 through 76 (raw steel mill products). This distinction matters significantly under the April 6th Section 232 overhaul.

For aluminum heat exchangers, the picture is clear. HTS subheadings 8419.50.10 and 8419.50.50 are explicitly listed as aluminum derivative articles in the April 6th proclamation, meaning imported finished aluminum heat exchangers are subject to a 25% tariff on the full customs value of the unit. Not just the metal content. On a $500,000 imported aluminum heat exchanger, the tariff base is the full $500,000.

For stainless steel, alloy, and carbon steel heat exchangers, and for pressure vessels of any material, the situation is less settled. These products typically classify under HTS 8419.50.50 and 8419.89, respectively, neither of which appears in the steel derivatives section of the April 6th annexes. This creates a genuine gray area. Imported finished steel heat exchangers and pressure vessels may not currently be explicitly covered by the Section 232 derivative tariff on the finished unit.

It is also worth noting what the Annex language does and does not say about tanks and vessels under Chapter 73. Two codes are listed under Annex I-A at the 50% rate. HTS 7309.00.00 covers iron or steel reservoirs, tanks, vats, and similar containers with a capacity exceeding 300 liters, but only those not fitted with mechanical or thermal equipment. HTS 7311.00.00 covers iron or steel containers for compressed or liquefied gas.

While these codes may appear to cover pressure vessels at first glance, the critical limitation in 7309 is the phrase: “not fitted with mechanical or thermal equipment.” A fabricated ASME pressure vessel with nozzles, instrumentation, internals, and process connections would almost certainly not qualify under that language. Neither code uses the word “vessel” at all. A purpose-engineered ASME Code vessel is fundamentally different from a simple storage tank or container. The customs classification of fabricated pressure equipment under Chapter 73 versus Chapter 84 is a fact-specific determination, and Chapter 84 typically governs process equipment of this nature.

What is unambiguous for all product types is that the raw material inputs (i.e. stainless plate, carbon steel plate, seamless and welded tubing, and pipe fittings) are covered at the full 50% rate under Annex I-A, regardless of how the finished equipment is ultimately classified.

One Process Change Worth Noting

The petition-based inclusion process that previously allowed domestic manufacturers and trade associations to formally request that specific HTS codes be added to Section 232 scope has been terminated. Going forward, Commerce and USTR will adjust product coverage on a rolling basis at their own discretion. There is no formal submission window anymore.

That means if you believe imported finished pressure vessels and heat exchangers should be explicitly covered under Section 232 derivative tariffs, the path forward is direct engagement with your elected officials. Not a petition. A phone call. A meeting. A letter.

As pressure vessel and heat exchanger fabricators, we need to continue pushing for protection to be in place for manufacturers of steel products, not just for domestic suppliers of raw material. We encourage every customer and partner in this industry to make that contact.

What This Means for Ward

Nothing changes in our cost structure today. We purchase 80 to 90 percent of our material domestically depending on the project. Our total material spend has increased approximately 10 to 20 percent since Section 232 tariffs were enacted, resulting in a 5 to 15 percent overall unit price increase after labor. We are absorbing what we can, and we are passing through what we must.

We will continue to monitor the evolving situation and update you each month on the latest developments.

The administration has published several tariff fact sheets on the White House website (click here) as the tariff topic has evolved.

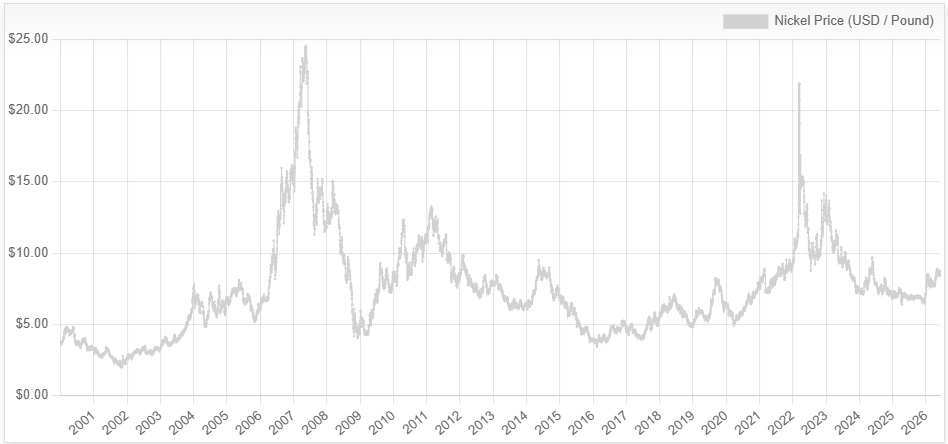

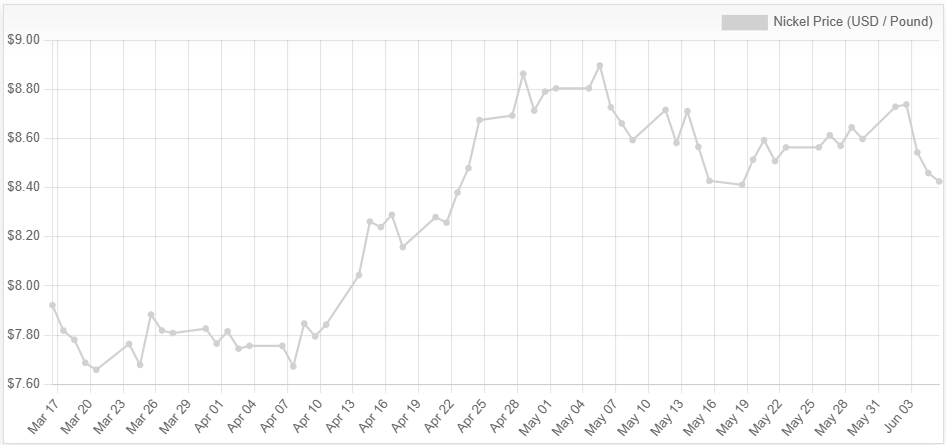

Nickel futures traded around $8.391 per pound, retreating sharply from above $8.718 to their lowest level in over a month, as investors locked in profits. Additional pressure came from sluggish nickel salt transactions in China and rising inventories, reflecting softer near-term demand. However, losses were limited by ongoing supply concerns in Indonesia, where Weda Bay Nickel suspended ore production after exhausting its reduced 2026 mining quota. The company is seeking an extension after receiving an initial allowance of 12 million wet metric tons this year, sharply below the 42 million tons produced in 2025, reinforcing concerns over ore availability. Investors also monitored regulatory changes in Indonesia, including tighter mining quotas and proposed tax measures that have raised concerns about future nickel supply growth. At the same time, India is preparing incentives for domestic nickel processing, highlighting expectations for longer-term growth in battery-material demand.

Plate mill plate lead times (weeks):

Domestic:

Stainless & Duplex: 12 to 13 (previously 10 to 11)

Nickel Alloys: 4 to 14 (previously 9 to 14)

Carbon steel: 13 to 17 (previously 9 to 13)

*Keep in mind, some plates will exceed the estimated ranges depending on the mill’s production schedule and slab availability. *

Welded tubing lead times (weeks):

Domestic:

Carbon: 6 to 16 (no change)

Stainless: 8 to 18 (previously 8 to 15)

Nickel Alloy: 8 to 18 (no change)

Import:

Carbon: 14 to 25 (no change)

Stainless: 16 to 30 (no change)

Nickel Alloy: 16 to 42 (no change)

Seamless tubing lead times (weeks):

Domestic:

Carbon: 6 to 26 (no change)

Stainless: 8 to 26 (no change)

Nickel Alloy: 8 to 18 (no change)

*Lead times are accurate if bar is in stock. If not, lead times can increase to 44 weeks as most bars are of foreign melt. *

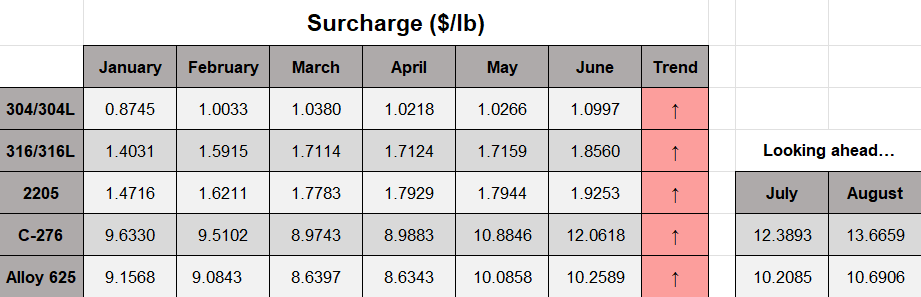

Nickel Prices have had an interesting ride over the past three decades, with a low of $2.20/lb. in October 2001 (following the September 11 events) and a high of $23.72/lb. in May 2007. Surcharges trail Nickel prices by approximately two months, so they would have been at their lowest in December 2001 (304 was $0.0182/lb.) and peak in July 2007 (304 was $2.2839/lb.).