In October 2023, the ISM Manufacturing Index (PMI) decreased to 46.7, down from the 10-month high of 49 in the previous month, falling significantly below the expected value of 49. A PMI reading above 50 means expansion, while below 50 means contraction. Therefore, this month’s value indicates the eleventh consecutive contraction in the US manufacturing sector. The data highlights the impact of the Federal Reserve’s higher borrowing costs on the industry, which is further testing the resilience of US goods producers, as observed in other reports. The decline in new orders accelerated to 45.5 from 49.2 in September, marking the 14th consecutive decline. Panelists mentioned reduced demand from both domestic and international markets. As a result, production slowed to 50.4 from 52.5, with growth nearly coming to a standstill, mainly due to a decrease in the backlog of orders (42.2 from 42.4) offsetting the decline in demand for new products. Additionally, employment contracted compared to the previous month’s rebound as factories reduced their capacity requirements. Furthermore, input prices fell for the sixth consecutive month, although the rate of decline was somewhat slower.

The Conference Board Consumer Confidence Index experienced a moderate decline in October, dropping to 102.6 (with a base of 1985=100) from a revised upward figure of 104.3 in September. The Present Situation Index, which reflects consumers’ views on current business and labor market conditions, decreased from 146.2 to 143.1. Meanwhile, the Expectations Index, which indicates consumers’ short-term outlook on income, business, and labor market conditions, saw a slight dip to 75.6 in October, following a decline to 76.4 in September. Notably, the Expectations Index is still below 80, a historical threshold signaling a potential recession within the next year. Consumer concerns about an imminent recession remain high, aligning with our expectations of a short and mild economic contraction in the first half of 2024.

“Consumer confidence fell again in October 2023, marking three consecutive months of decline,” said Dana Peterson, Chief Economist at The Conference Board. “October’s retreat reflected pullbacks in both the Present Situation and Expectations Index. Write-in responses showed that consumers continued to be preoccupied with rising prices in general, and for grocery and gasoline prices in particular. Consumers also expressed concerns about the political situation and higher interest rates. Worries around war/conflicts also rose, amid the recent turmoil in the Middle East. The decline in consumer confidence was evident across householders aged 35 and up, and not limited to any one income group.”

WTI Oil entered October at $87.170 per barrel. Prices peaked for the month on the 19th at $88.370 per barrel then trended down for the remainder of the month, closing at $81.020 per barrel. Oil prices have returned to their pre-attack levels before the conflict involving Hamas and Israel on October 7th. Concerns about disruptions to the oil supply in the Middle East have eased. However, the demand outlook for oil remains pessimistic. The ISM Services PMI in the US fell more than expected, and in China, the largest importer of oil, the manufacturing sector returned to a state of contraction while the services sector showed only slight growth. Additionally, US crude stockpiles increased for a second consecutive week. Meanwhile, it is anticipated that Saudi Arabia will reaffirm its commitment to extend its voluntary reduction in oil output by 1 million barrels per day through December.

The online US Oil Rig Count is at 618 which is down 7 compared to last month’s report and down 152 from Nov 4 of 2022. This key and leading indicator shows the current demand for products used in drilling, completing, producing, and processing hydrocarbons which all of us use every day as fuel sources and finished products. The number of rigs conducting oil and gas drilling in the United States continues to decrease. This decline in the U.S. rig count has occurred in 10 out of the last 11 weeks. Even the Permian Basin, which is the most productive region for oil and gas production in America, has experienced a drop in the number of operating rigs, with 337 currently compared to 342 last week and 350 a year ago.

This trend reflects the priority of drillers to focus on enhancing shareholder returns rather than expanding production coupled by the current administration’s desire to move away from fossil fuels. Additionally, there is uncertainty surrounding the economic outlook, leading the industry to remain cautious, especially compared to pre-pandemic times when the rig count showed a slower recovery over the past few years. To provide context, in 2019, there were 954 rigs drilling for oil and gas in the U.S. and, in 2014, there were 1609 rigs before oil prices dropped below $20 per barrel at the end of that year.

However, solid oil prices will likely prevent the rig count from decreasing significantly and may even lead to a rebound later this year. Currently, the West Texas Intermediate benchmark prices have been at around $75 per barrel, which is sufficient for most drillers to be profitable. Consequently, the U.S. is still expected to set a new annual oil production record in 2023, with a projected 12.4 million barrels per day, slightly surpassing the 2019 record of 12.3 million bpd.

Nickel continued its downward slide we saw in September as we enter October at $8.385 per pound. Pricing continued to decrease, at a slower rate than in September, closing out the month at $8.121 per pound. We are experiencing a two year low amid a worsened demand outlook triggered by fears of elevated interest rates, as inflationary pressures persist. Simultaneously, the electric vehicle sector experienced a downturn, with manufacturers of batteries for new EVs gradually curtailing their input buying activity since the onset of the third quarter. Meanwhile, traders continued to assess the impact of China’s stimulus measures after the country’s official manufacturing PMI fell to 49.5 in October, underlining the economy’s fragile recovery. The metal found some support in the full-year nickel production guidance cuts by giant Glencore. Glencore lowered its forecast for 2023 nickel output by 9% to around 102,000 tons, mainly due to maintenance outages at the Sudbury smelter and a longer than expected recovery from the 2022 strike action. Still, the market faced the largest demand-supply surplus in at least a decade.

Below is the 90 day Nickel Price Trend (US$ per tonne).

Commodity stainless plate deliveries look to have pulled in again on certain grades and sizes to a 7 to 11 week range. Nickel alloy plates held at the 11 to 15 week range. Duplex plates are currently sitting in the 11 to 12 week range. Carbon steel plate mill deliveries continue to reside in the 8 to 11 week delivery range. Remember that some plates will exceed the estimated ranges depending on the mill’s schedule.

Welded tubing – Currently deliveries for domestically welded stainless tubing are in the 8 to 12 week range, whether small or large quantities (Up to 26 weeks for import). Carbon steel tubing deliveries have lead times ranging anywhere from 8 to 12 weeks when strip is available. Welded nickel alloy tubing ranges from 8 to 14 weeks (up to 42 weeks for imports). There has been a decrease across the board in tubing lead times as domestic mills are looking for more work.

Seamless tubing – Current schedules reflect 10 to 20 weeks or more for carbon steel (24 to 26 weeks for Western European carbon seamless) and 10 to 35 weeks for stainless. Seamless nickel tubing is being offered at the 10 to 14 week delivery window so long as hollows are in stock. If hollows are not readily available, anticipate deliveries of seamless nickel tubing in the 20 to 32 week timeframe.

Please don’t hesitate to reach out if you have any questions about the current state of our industry’s material supply chain.

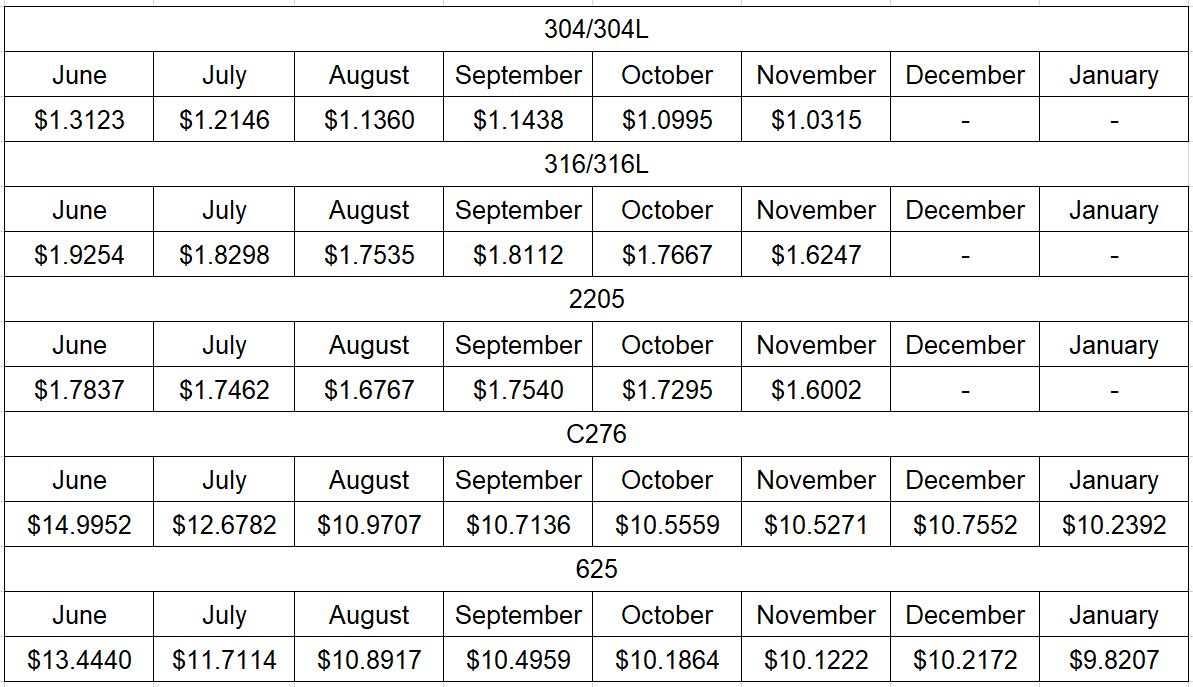

Here’s the current surcharge chart for 304/304LSS, 316/316LSS, 2205, C276, and 625.

Nickel Prices have had an interesting ride over the past two decades with a low of $2.20/lb. in October of 2001 (following September 11 events) and a high of $23.72/lb. in May of 2007. Surcharges trail Nickel prices by approximately two months, so they would have been at their lowest in December of 2001 (304 was $0.0182/lb.) with the peak in July of 2007 (304 was $2.2839/lb.).

The chart below illustrates Nickel price by way of U.S. Dollars per Metric ton.

Here’s the Price Index for Hot Rolled Bars, Plate, and Structural Shapes.